import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import timeSupervised Learning

Introduction

Data pre-processing

Data

The dataset used in this part is the Bank Marketing from the UC Irvine Machine Learning Repository. The data is licensed under CC BY, allowing it to be freely used for this exercise.

The dataset contains data from direct marketing campaigns (phone calls) of a Portuguese banking institution. The data comprises 16 features and a labelled variable, “y”, which indicates if the client subscribed to a term deposit.

Load data

The data is loaded into a pandas dataframe from the downloaded CSV file. After loading the data, the first five rows of the dataframe are inspected using the head() function. The dataframe is then checked for any missing values. This dataset is clean with no missing values.

# Load the data file into a dataframe

bank_df = pd.read_csv("bank-full.csv", sep=";", comment="#")

# Inspect the head of the data

print(bank_df.head()) age job marital education default balance housing loan \

0 58 management married tertiary no 2143 yes no

1 44 technician single secondary no 29 yes no

2 33 entrepreneur married secondary no 2 yes yes

3 47 blue-collar married unknown no 1506 yes no

4 33 unknown single unknown no 1 no no

contact day month duration campaign pdays previous poutcome y

0 unknown 5 may 261 1 -1 0 unknown no

1 unknown 5 may 151 1 -1 0 unknown no

2 unknown 5 may 76 1 -1 0 unknown no

3 unknown 5 may 92 1 -1 0 unknown no

4 unknown 5 may 198 1 -1 0 unknown no Check for null values

# Check how many null values are in the data frame

print()

print("Feature Name Number of missing entries")

print(bank_df.isnull().sum())

Feature Name Number of missing entries

age 0

job 0

marital 0

education 0

default 0

balance 0

housing 0

loan 0

contact 0

day 0

month 0

duration 0

campaign 0

pdays 0

previous 0

poutcome 0

y 0

dtype: int64Check for duplicate values

# Count duplicate rows

duplicate_count = bank_df.duplicated().sum()

print(f"Number of duplicate rows: {duplicate_count}")Number of duplicate rows: 0Drop irrelevant features

The dataset metadata states that the “duration” feature should only be included for benchmark purposes and should be discarded if the intention is to have a realistic predictive model.

bank_df.drop(["duration"], axis=1, inplace=True)Feature encoding

The source of the dataset provides information relating to each variable, such as data type.

from sklearn.preprocessing import LabelEncoder

from sklearn.preprocessing import OneHotEncoderCheck datatypes

bank_df.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 45211 entries, 0 to 45210

Data columns (total 16 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 age 45211 non-null int64

1 job 45211 non-null object

2 marital 45211 non-null object

3 education 45211 non-null object

4 default 45211 non-null object

5 balance 45211 non-null int64

6 housing 45211 non-null object

7 loan 45211 non-null object

8 contact 45211 non-null object

9 day 45211 non-null int64

10 month 45211 non-null object

11 campaign 45211 non-null int64

12 pdays 45211 non-null int64

13 previous 45211 non-null int64

14 poutcome 45211 non-null object

15 y 45211 non-null object

dtypes: int64(6), object(10)

memory usage: 5.5+ MBCheck categorical features

# List of columns to inspect

selected_columns = ["job", "marital", "education", "default", "housing", "loan", "contact", "month", "poutcome"]

# Print unique values for each selected column

for column in selected_columns:

unique_values = bank_df[column].unique()

print(f"Unique values in column '{column}':")

print(unique_values)

print("-" *70)Unique values in column 'job':

['management' 'technician' 'entrepreneur' 'blue-collar' 'unknown'

'retired' 'admin.' 'services' 'self-employed' 'unemployed' 'housemaid'

'student']

----------------------------------------------------------------------

Unique values in column 'marital':

['married' 'single' 'divorced']

----------------------------------------------------------------------

Unique values in column 'education':

['tertiary' 'secondary' 'unknown' 'primary']

----------------------------------------------------------------------

Unique values in column 'default':

['no' 'yes']

----------------------------------------------------------------------

Unique values in column 'housing':

['yes' 'no']

----------------------------------------------------------------------

Unique values in column 'loan':

['no' 'yes']

----------------------------------------------------------------------

Unique values in column 'contact':

['unknown' 'cellular' 'telephone']

----------------------------------------------------------------------

Unique values in column 'month':

['may' 'jun' 'jul' 'aug' 'oct' 'nov' 'dec' 'jan' 'feb' 'mar' 'apr' 'sep']

----------------------------------------------------------------------

Unique values in column 'poutcome':

['unknown' 'failure' 'other' 'success']

----------------------------------------------------------------------Encoding nominal categorical features

The categorical features require encoding. One-hot encoding was applied to the nominal features: “job”, “marital”, “contact”, “month”, “default”, “housing”, “loan” and “poutcome”.

# Columns to encode

one_hot_cols = ["job", "marital", "default", "housing", "loan", "contact", "month", "poutcome"]

# OneHotEncoder setup

encoder = OneHotEncoder(sparse_output=False)

encoded = encoder.fit_transform(bank_df[one_hot_cols])

# Create DataFrame from encoded data

encoded_df = pd.DataFrame(encoded, columns=encoder.get_feature_names_out(one_hot_cols))

print(encoded_df.head())

#Copy the bank dataframe

en_bank_df= bank_df.copy()

# Drop original columns

en_bank_df = en_bank_df.drop(one_hot_cols, axis=1)

# Insert encoded columns before the last column

insert_position = en_bank_df.shape[1] - 1

for col in reversed(encoded_df.columns):

en_bank_df.insert(insert_position, col, encoded_df[col]) job_admin. job_blue-collar job_entrepreneur job_housemaid \

0 0.0 0.0 0.0 0.0

1 0.0 0.0 0.0 0.0

2 0.0 0.0 1.0 0.0

3 0.0 1.0 0.0 0.0

4 0.0 0.0 0.0 0.0

job_management job_retired job_self-employed job_services job_student \

0 1.0 0.0 0.0 0.0 0.0

1 0.0 0.0 0.0 0.0 0.0

2 0.0 0.0 0.0 0.0 0.0

3 0.0 0.0 0.0 0.0 0.0

4 0.0 0.0 0.0 0.0 0.0

job_technician ... month_jun month_mar month_may month_nov month_oct \

0 0.0 ... 0.0 0.0 1.0 0.0 0.0

1 1.0 ... 0.0 0.0 1.0 0.0 0.0

2 0.0 ... 0.0 0.0 1.0 0.0 0.0

3 0.0 ... 0.0 0.0 1.0 0.0 0.0

4 0.0 ... 0.0 0.0 1.0 0.0 0.0

month_sep poutcome_failure poutcome_other poutcome_success \

0 0.0 0.0 0.0 0.0

1 0.0 0.0 0.0 0.0

2 0.0 0.0 0.0 0.0

3 0.0 0.0 0.0 0.0

4 0.0 0.0 0.0 0.0

poutcome_unknown

0 1.0

1 1.0

2 1.0

3 1.0

4 1.0

[5 rows x 40 columns]Encoding ordinal categorical features

Ordinal encoding was applied to the ordinal feature “education”, as its ordering is important.

# Ordinal encoding

# Education ordinal mapping

education_mapping = {

"unknown": 0,

"primary": 1,

"secondary": 2,

"tertiary": 3

}

# Apply the mapping

en_bank_df["education"] = en_bank_df["education"].map(education_mapping)

# Display the updated dataframe with encoded columns.

print(en_bank_df[["education"]].head()) education

0 3

1 2

2 2

3 0

4 0Target encoding

# Create label encoder

le = LabelEncoder()

en_bank_df = en_bank_df.rename(columns={"y": "target"})

en_bank_df["target"] = le.fit_transform(en_bank_df["target"])

en_bank_df.head(5)| age | education | balance | day | campaign | pdays | previous | job_admin. | job_blue-collar | job_entrepreneur | ... | month_mar | month_may | month_nov | month_oct | month_sep | poutcome_failure | poutcome_other | poutcome_success | poutcome_unknown | target | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 58 | 3 | 2143 | 5 | 1 | -1 | 0 | 0.0 | 0.0 | 0.0 | ... | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0 |

| 1 | 44 | 2 | 29 | 5 | 1 | -1 | 0 | 0.0 | 0.0 | 0.0 | ... | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0 |

| 2 | 33 | 2 | 2 | 5 | 1 | -1 | 0 | 0.0 | 0.0 | 1.0 | ... | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0 |

| 3 | 47 | 0 | 1506 | 5 | 1 | -1 | 0 | 0.0 | 1.0 | 0.0 | ... | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0 |

| 4 | 33 | 0 | 1 | 5 | 1 | -1 | 0 | 0.0 | 0.0 | 0.0 | ... | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0 |

5 rows × 48 columns

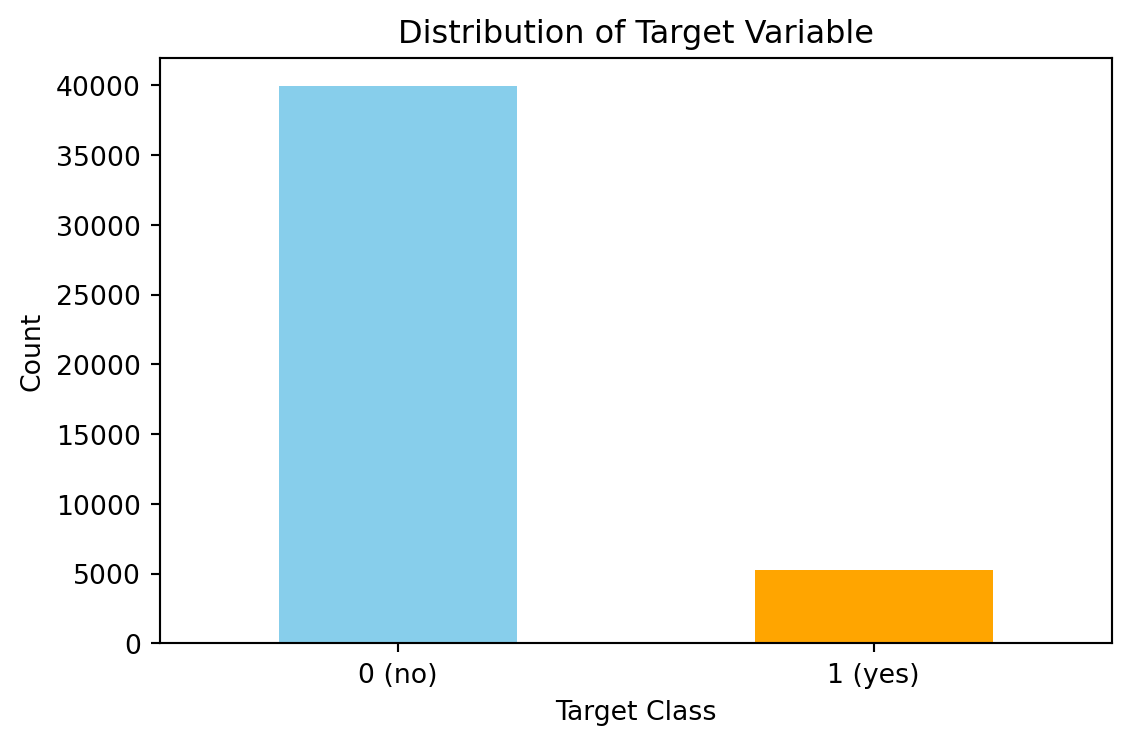

Dataset balance

Here I inspect the blance of the classes in the full dataset. The figure below shows there is many more no’s (0) and yes’s (1).

# Count distribution of 0s and 1s

target_counts = en_bank_df["target"].value_counts()

# Plot the distribution

plt.figure(figsize=(6, 4))

target_counts.plot(kind="bar", color=["skyblue", "orange"])

plt.title("Distribution of Target Variable")

plt.xlabel("Target Class")

plt.ylabel("Count")

plt.xticks(ticks=[0, 1], labels=["0 (no)", "1 (yes)"], rotation=0)

plt.tight_layout()

plt.show()

Handling dataset imbalance

It has been observed that the dataset is imbalanced with approximately 11% of the data in the “yes” class and the remaining in the “no” class. There are several ways to handle imbalanced datasets, such as under-sampling the majority class, oversampling the minority class, SMOTE, and cost-sensitive learning, where the weights of each class are adjusted to adjust the cost function. I tested both SMOTE and found that the increased training set size caused problems with overfitting in the K-NN section. Therefore, here I have opted to use cost-sensitive learning.

Train test split

Stratified sampling has been used to ensure the class proporations remaing the same in the test and train sets.

from sklearn.model_selection import StratifiedShuffleSplit

from sklearn.preprocessing import StandardScaler

# Split the data

# Stratified sampling to help maintain similar distributions between the text and train sets

stratSplit = StratifiedShuffleSplit(n_splits=1, test_size=0.2, random_state=8)

for train_index, test_index in stratSplit.split(en_bank_df.iloc[:, :-1], en_bank_df["target"]):

X_train = en_bank_df.iloc[:, :-1].iloc[train_index]

X_test = en_bank_df.iloc[:, :-1].iloc[test_index]

y_train = en_bank_df["target"].iloc[train_index]

y_test = en_bank_df["target"].iloc[test_index]

# Fit scaler on training data

scaler = StandardScaler()

X_train_scald = scaler.fit_transform(X_train)

# Transform test data using the same scaler

X_test_scald = scaler.transform(X_test)

# check class distribution in test set

test_counts = y_test.value_counts()

# check null accuracy score

null_accuracy = (test_counts[0]/(test_counts[0] + test_counts[1]))

print(f"Null accuracy score: {null_accuracy:.4f}")Null accuracy score: 0.8830First logistic regression (no regularisation)

Here, a logistic regression model is fitted without any regularisation. The logistic regression model in scikit learn has several hyperparameters. Those specific to the non-regularised version are:

- Solver: The type of solver used.

- Maximum Iterations: Controls how long the solver runs.

- Tolerance: Determines the stopping criteria for the optimisation.

- Class Weight: Useful for imbalanced datasets.

Since I will be creating regularised logistic models for this data later, I decided to remove the solver from the hyperparameter tuning. There is only one solver (“saga”) that handles no regularisation and the L1 and L2 regularisation, and I want to use the same solver for each model.

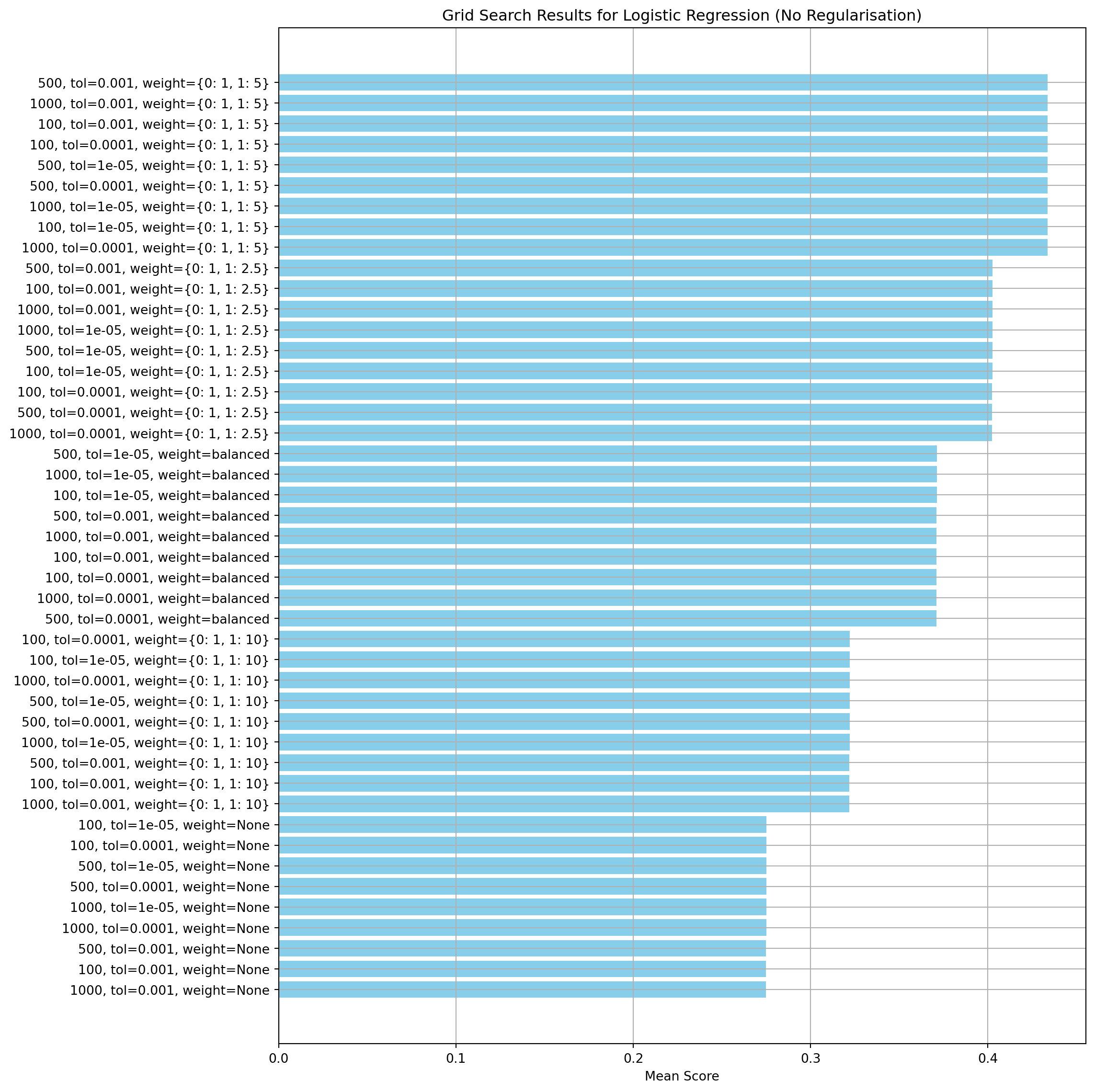

Hyperparameter tuning

For the model evaluation, I have used the F1 score. F1 is the harmonic mean of precision and recall. The main objective of this modelling work is to predict whether a customer will subscribe to a term deposit. Therefore, I aim to strike a balance between the recall (don’t want to miss potential conversions) and the precision (don’t want to waste effort on uninterested people).

The scikit learn GridSearchCV is used to execute the parameter tuning. It runs through all combinations of the parameters and uses cross-validation to assess the performance of the model. The results showed that the maximum number of iterations and convergence tolerance were not significant compared to the class weights.

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import GridSearchCV

from sklearn.pipeline import Pipeline

# Define pipeline (logistic regression)

pipeline = Pipeline([

("logreg", LogisticRegression(penalty=None, solver="saga", random_state=8))

])

param_grid = {

"logreg__class_weight": [

None,

'balanced',

{0: 1, 1: 2.5},

{0: 1, 1: 5},

{0: 1, 1: 10}

],

"logreg__max_iter": [100, 500, 1000],

"logreg__tol": [1e-5, 1e-4, 1e-3],

}

# Set up GridSearchCV

# GridSearchCV uses stratified sampling internally, so need to do anything special here.

# Only interested in minorty class so don't weight score

grid_search = GridSearchCV(pipeline, param_grid, cv=5, scoring="f1", n_jobs=-1, return_train_score=True)

# Fit the model

grid_search.fit(X_train_scald, y_train)

# Convert results to DataFrame

results_df = pd.DataFrame(grid_search.cv_results_)

# Create a readable label for each parameter combination

results_df["param_combo"] = results_df.apply(

lambda row: f"{row['param_logreg__max_iter']}, tol={row['param_logreg__tol']}, weight={row['param_logreg__class_weight']}",

axis=1

)

# Sort by mean test score

results_df = results_df.sort_values(by="mean_test_score", ascending=False)

# Plot performance of each combination in grid search

plt.figure(figsize=(12, 12))

plt.barh(results_df["param_combo"], results_df["mean_test_score"], color="skyblue")

plt.xlabel("Mean Score")

plt.title("Grid Search Results for Logistic Regression (No Regularisation)")

plt.gca().invert_yaxis()

plt.tight_layout()

plt.grid(True)

plt.show()

# Best parameters and score

print("Best Parameters:", grid_search.best_params_)

print(f"Best Score: {grid_search.best_score_:.4f}")

Best Parameters: {'logreg__class_weight': {0: 1, 1: 5}, 'logreg__max_iter': 100, 'logreg__tol': 0.001}

Best Score: 0.4336Create a model with the best parameters and run cross-validation

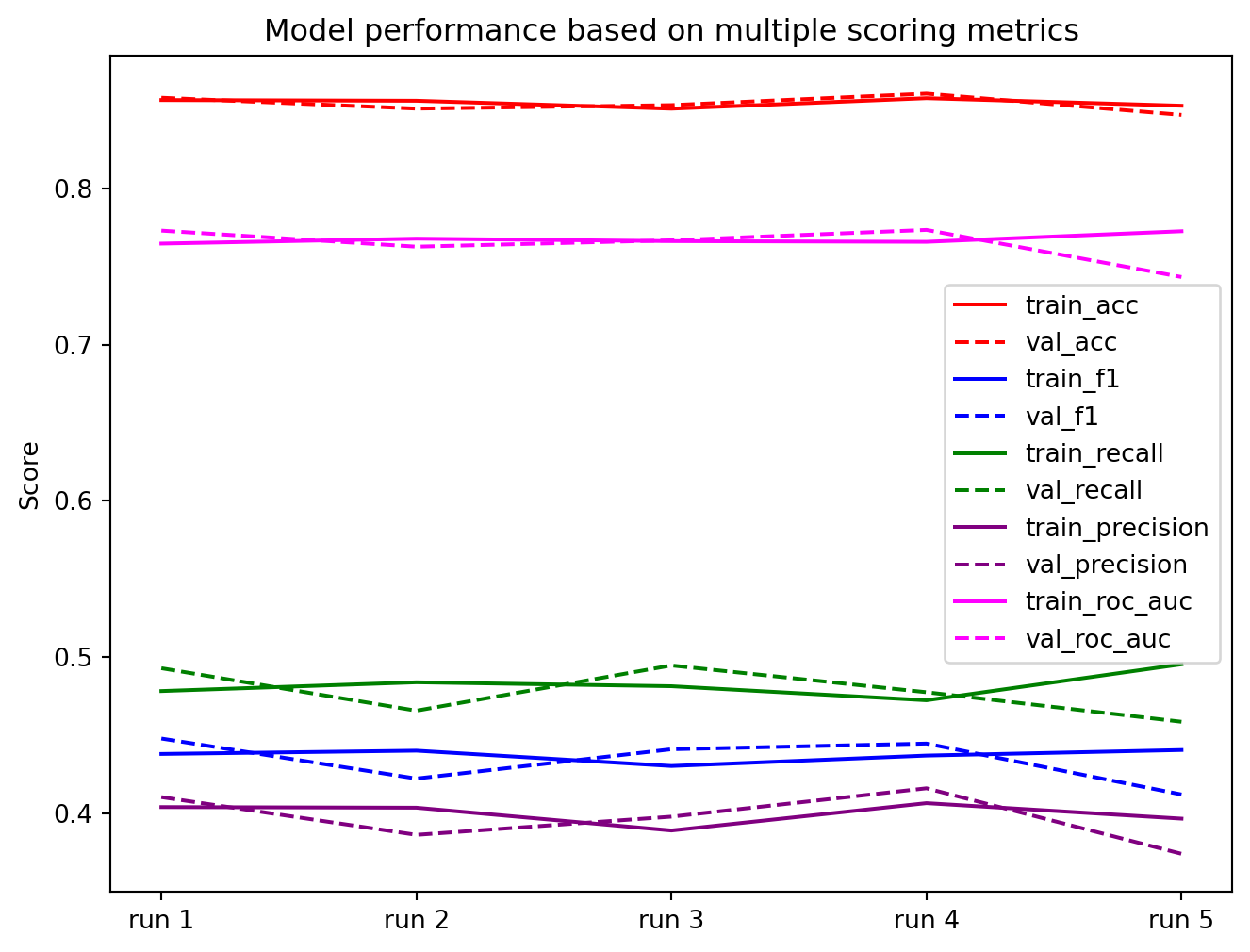

Here, I’m using cross-validation to check the model’s ability to generalise. Looking for divergence between the training and validation scores. The results show the model is stable and not over-fitted.

from sklearn.model_selection import cross_validate

def performCV(model, X_train, y_train):

"""

Function to perform cross-validation for a given model and training data.

:param model: The model to validate.

:param X_train: Training data.

:param y_train: TRaining labels.

:returns: Dictionary of results from the cross-validation.

"""

results = cross_validate(model, X=X_train, y=y_train,

scoring=["f1", "precision", "recall", "accuracy", "roc_auc"],

cv=5, verbose=True, return_train_score=True,

return_estimator=True)

return results

def visualiseResults(results):

"""

Function to plot different scoring metrics from a cross-validsation

study.

:param results: Dictionary containing the cross-validation results.

:returns: None.

"""

cvData = {"val_f1":results["test_f1"],

"train_f1":results["train_f1"],

"val_precision":results["test_precision"],

"train_precision":results["train_precision"],

"val_recall":results["test_recall"],

"train_recall":results["train_recall"],

"val_acc":results["test_accuracy"],

"train_acc":results["train_accuracy"],

"val_roc_auc":results["test_roc_auc"],

"train_roc_auc":results["train_roc_auc"]}

cv_df = pd.DataFrame(cvData)

fig = plt.figure(figsize=(8,6))

ax = fig.add_subplot()

plt.plot(cv_df.index, cv_df["train_acc"], label="train_acc", color="r")

plt.plot(cv_df.index, cv_df["val_acc"], label="val_acc", c="r", ls="--")

plt.plot(cv_df.index, cv_df["train_f1"], label="train_f1", c="b")

plt.plot(cv_df.index, cv_df["val_f1"], label="val_f1", c="b", ls="--")

plt.plot(cv_df.index, cv_df["train_recall"], label="train_recall", c="g")

plt.plot(cv_df.index, cv_df["val_recall"], label="val_recall", c="g", ls="--")

plt.plot(cv_df.index, cv_df["train_precision"], label="train_precision", c="purple")

plt.plot(cv_df.index, cv_df["val_precision"], label="val_precision", c="purple", ls="--")

plt.plot(cv_df.index, cv_df["train_roc_auc"], label="train_roc_auc", c="magenta")

plt.plot(cv_df.index, cv_df["val_roc_auc"], label="val_roc_auc", c="magenta", ls="--")

plt.legend()

plt.ylabel("Score")

plt.title("Model performance based on multiple scoring metrics")

plt.xticks(range(len(results["fit_time"])),["run "+str(i+1) for i in range(len(results["fit_time"]))])

plt.show()# Create the model using the best parameters found in the hyperparameter tuning step

log_reg_nr = LogisticRegression(penalty=None, solver="saga", max_iter=400, tol=0.001, class_weight={0: 1, 1: 5}, random_state=8)

# Run cross-validation

cv_results = performCV(log_reg_nr, X_train_scald, y_train)

visualiseResults(cv_results)[Parallel(n_jobs=1)]: Done 5 out of 5 | elapsed: 1.1s finished

Evaluate model performance

Here, I evaluate the model’s performance by calculating the precision, recall, F1 score and the ROC_AUC score. The confusion matrix is also plotted. The recall and precision are very good for the majority class, as expected, due to the class imbalance. The minority class shows the precision is approximately 42% and the recall is approximately 50%.

from sklearn.metrics import classification_report

from sklearn.metrics import confusion_matrix, ConfusionMatrixDisplay

from sklearn.metrics import roc_auc_score

log_reg_nr.fit(X_train_scald, y_train)

y_pred = log_reg_nr.predict(X_test_scald)

print(classification_report(y_test, y_pred, target_names=["no", "yes"], digits=4))

# Predict probabilities

y_probs = log_reg_nr.predict_proba(X_test_scald)[:, 1] # Probabilities for class 1

# Compute ROC AUC

roc_auc = roc_auc_score(y_test, y_probs)

print(f"ROC AUC Score: {roc_auc:.4f}")

cm_nr = confusion_matrix(y_test, y_pred, labels=[0,1]) precision recall f1-score support

no 0.9319 0.9088 0.9202 7985

yes 0.4204 0.4991 0.4564 1058

accuracy 0.8609 9043

macro avg 0.6762 0.7039 0.6883 9043

weighted avg 0.8721 0.8609 0.8660 9043

ROC AUC Score: 0.7735Second and Third logistic regression models

In this second two additional logistic regission models are created with differing regularisation to invesitigate if regularisation affects the performance of the model for this application.

LASSO regularisation (L1)

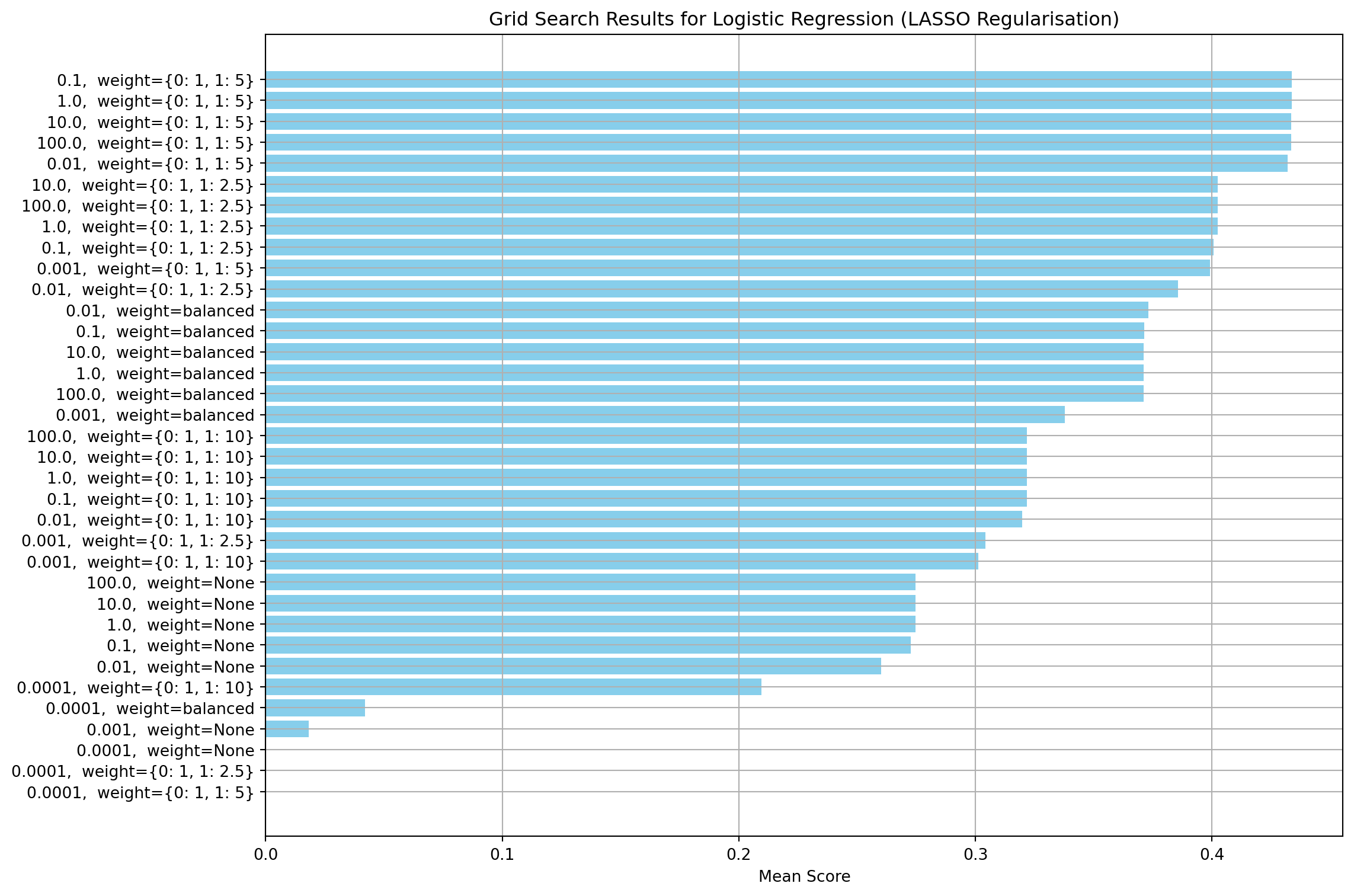

This section creates a regularisation model using the L1 norm. Firstly, I run a grid search to find the value of C and the class weights that give the highest F1 score. Other parameters, such as convergence tolerance, maximum solver iterations and class weights have been set to the same values used for the non-regularised model. Like the non-regularised model, the class weights have the most effect on the model performance. The value of the regularisation strength (C) has little effect once the optimal class weights are selected.

# LASSO - L1

# Define pipeline

lasso_pipeline = Pipeline([

("lasso", LogisticRegression(penalty="l1", solver="saga", random_state=8,

tol=1e-3, max_iter=400, class_weight=None))

])

# Define parameter grid

lasso_params = {

"lasso__C": [0.0001, 0.001, 0.01, 0.1, 1.0, 10.0, 100.0],

"lasso__class_weight": [

None,

'balanced',

{0: 1, 1: 2.5},

{0: 1, 1: 5},

{0: 1, 1: 10}

]

}

# Set up GridSearchCV

lasso_grid_search = GridSearchCV(lasso_pipeline, lasso_params, cv=5, scoring="f1", n_jobs=-1, return_train_score=True)

# Fit the model

lasso_grid_search.fit(X_train_scald, y_train)

# Convert results to DataFrame

lasso_results_df = pd.DataFrame(lasso_grid_search.cv_results_)

# Create a readable label for each parameter combination

lasso_results_df["param_combo"] = lasso_results_df.apply(

lambda row: f"{row['param_lasso__C']}, weight={row['param_lasso__class_weight']}",

axis=1

)

# Sort by mean test score

lasso_results_df = lasso_results_df.sort_values(by="mean_test_score", ascending=False)

# Plot performance of each combination in grid search

plt.figure(figsize=(12, 8))

plt.barh(lasso_results_df["param_combo"], lasso_results_df["mean_test_score"], color="skyblue")

plt.xlabel("Mean Score")

plt.title("Grid Search Results for Logistic Regression (LASSO Regularisation)")

plt.gca().invert_yaxis()

plt.tight_layout()

plt.grid(True)

plt.show()

# Best parameters and score

print("Best Parameters:", lasso_grid_search.best_params_)

print(f"Best Score: {lasso_grid_search.best_score_:.4f}")

Best Parameters: {'lasso__C': 0.1, 'lasso__class_weight': {0: 1, 1: 5}}

Best Score: 0.4337log_reg_l1 = LogisticRegression(penalty="l1", solver="saga", max_iter=400, tol=0.001, class_weight= {0: 1, 1: 5}, C=0.1)Ridge regularisation (L2)

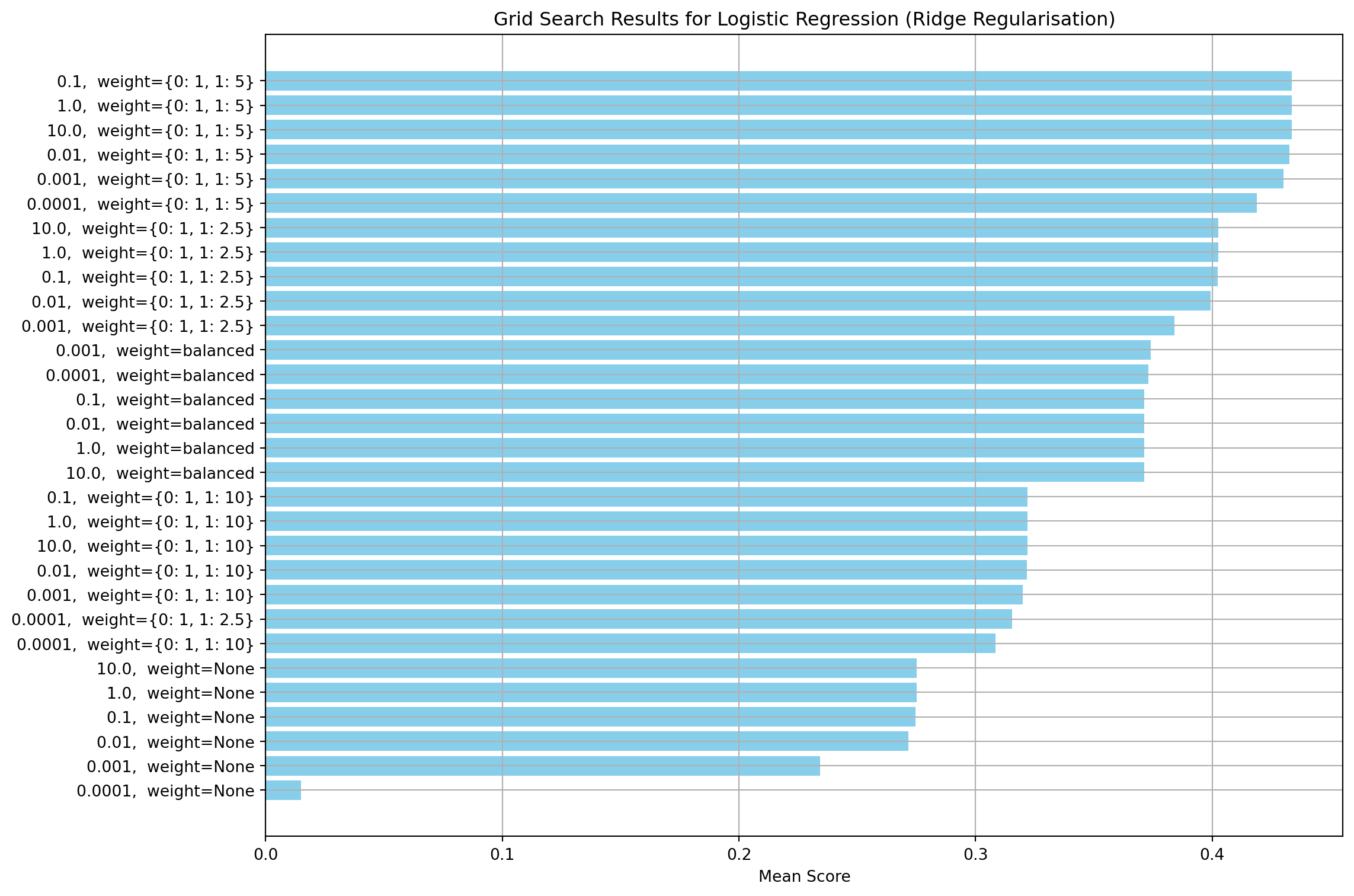

This section creates a regularisation model using the L2 norm. Firstly, I run a grid to find the values of C and class weights that give the highest F1 score. Other parameters, such as convergence tolerance, maximum solver iterations and class weights have been set to the same values used for the non-regularised model. Similar to the other two models, the class weights are the most important parameter. The regularisation strength has no effect for values about 0.1

# Ridge - L2

# Define pipeline

ridge_pipeline = Pipeline([

("ridge", LogisticRegression(penalty="l2", solver="saga", random_state=8,

tol=1e-5, max_iter=100, class_weight=None))

])

# Define parameter grid

ridge_params = {

"ridge__C": [0.0001, 0.001, 0.01, 0.1, 1.0, 10.0],

"ridge__class_weight": [

None,

'balanced',

{0: 1, 1: 2.5},

{0: 1, 1: 5},

{0: 1, 1: 10}

]

}

# Set up GridSearchCV

ridge_grid_search = GridSearchCV(ridge_pipeline, ridge_params, cv=5, scoring="f1", n_jobs=-1, return_train_score=True)

# Fit the model

ridge_grid_search.fit(X_train_scald, y_train)

# Convert results to DataFrame

ridge_results_df = pd.DataFrame(ridge_grid_search.cv_results_)

# Create a readable label for each parameter combination

ridge_results_df["param_combo"] = ridge_results_df.apply(

lambda row: f"{row['param_ridge__C']}, weight={row['param_ridge__class_weight']}",

axis=1

)

# Sort by mean test score

ridge_results_df = ridge_results_df.sort_values(by="mean_test_score", ascending=False)

# Plot performance of each combination in grid search

plt.figure(figsize=(12, 8))

plt.barh(ridge_results_df["param_combo"], ridge_results_df["mean_test_score"], color="skyblue")

plt.xlabel("Mean Score")

plt.title("Grid Search Results for Logistic Regression (Ridge Regularisation)")

plt.gca().invert_yaxis()

plt.tight_layout()

plt.grid(True)

plt.show()

# Best parameters and score

print("Best Parameters:", ridge_grid_search.best_params_)

print(f"Best Score: {ridge_grid_search.best_score_:.4f}")

Best Parameters: {'ridge__C': 0.1, 'ridge__class_weight': {0: 1, 1: 5}}

Best Score: 0.4337log_reg_l2 = LogisticRegression(penalty="l2", solver="saga", random_state=8,

max_iter=400, tol=1e-3, class_weight= {0: 1, 1: 5}, C=0.1)Comparsion of 1st, 2nd and 3rd models

In this section, I compare the performance of the three logistic models.

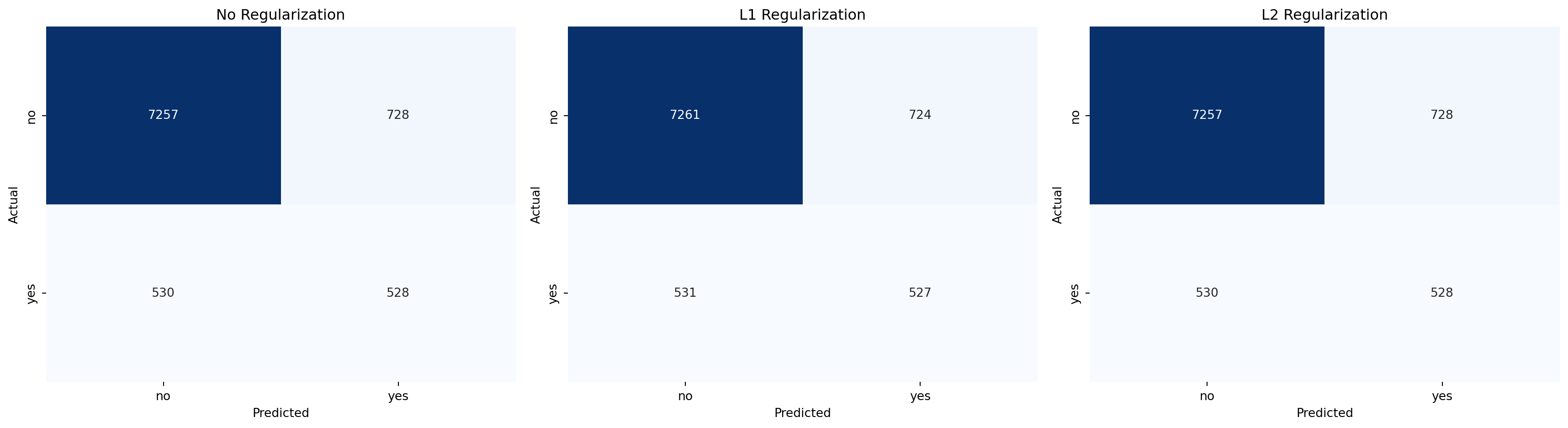

The performance metrics are virtually identical across all three models (differences in the third decimal place), which confirms that regularisation isn’t providing meaningful benefit here. This suggests the first model is already well-calibrated without regularisation. Since regularisation isn’t having any effect, the models are not overfitting. The logistic regression coefficients for each model have also been printed and compared.

Comparison Summary

| Model | Recall (yes) | Precision (yes) | F1 Score (yes) | ROC_AUC score (yes) |

|---|---|---|---|---|

| No Regularization | 0.4991 | 0.4564 | 0.4204 | 0.7735 |

| L1 Regularization | 0.4981 | 0.4565 | 0.4213 | 0.7738 |

| L2 Regularization | 0.4991 | 0.4565 | 0.4204 | 0.7736 |

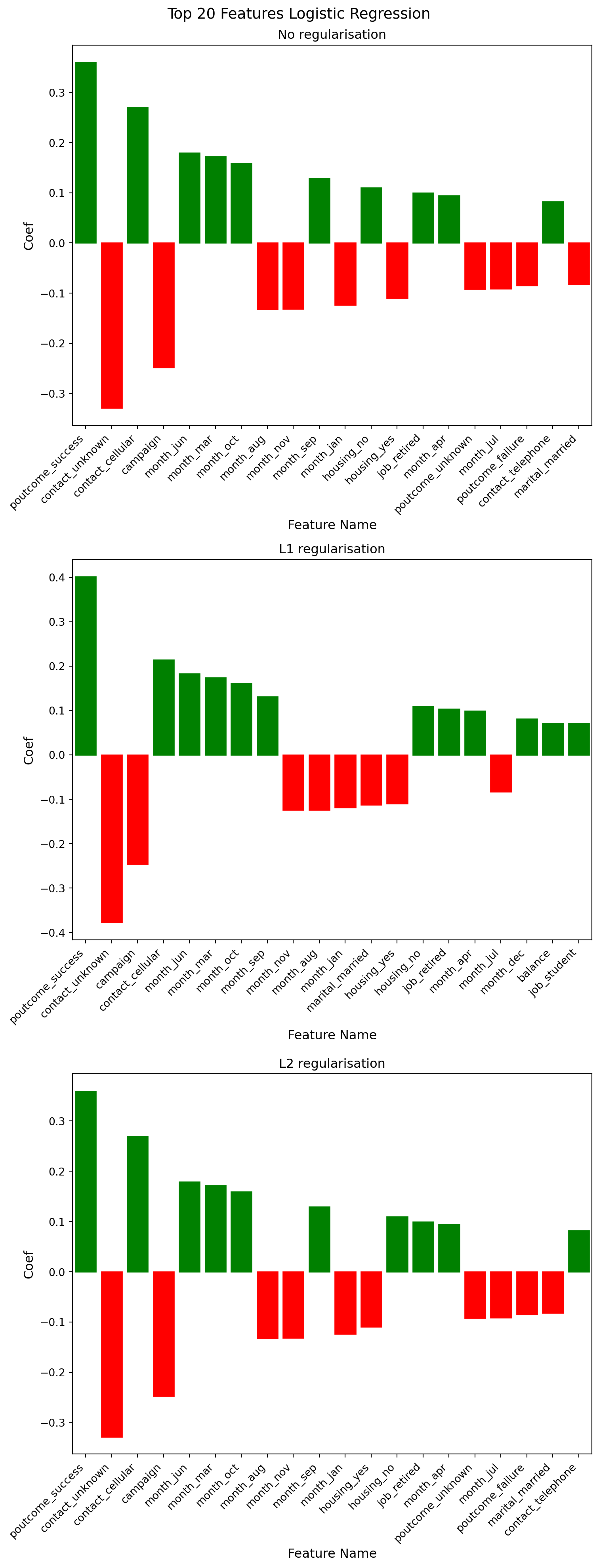

The coefficients are remarkably similar across all three models (no regularisation, L1, and L2), which suggests:

- Model Stability - The fact that regularisation barely changes the coefficients suggests the first model wasn’t significantly overfitting. If there were overfitting, I’d expect to see much larger differences when regularisation is applied.

- Feature importance is consistent between the non-regularised and L2 models. The first two largest coefficients are consistent across all models:

- poutcome_sucess: ~0.36 (strongest positive predictor)

- contact_unknown: ~-0.33 (strongest negative predictor)

- L1 vs L2 Differences - L1 regularisation typically drives some coefficients to exactly zero (feature selection), while L2 shrinks them toward zero. The L1 model is driving four coefficients to zero, which reinforces that most features are contributing meaningful information.

import matplotlib.pyplot as plt

import seaborn as sns

import numpy as np

# Define confusion matrices based on the provided metrics

# L1 regularization

log_reg_l1.fit(X_train_scald, y_train)

y_pred_l1 = log_reg_l1.predict(X_test_scald)

cm_l1 = confusion_matrix(y_test, y_pred_l1, labels=[0,1])

print("L1 regularisation results:")

print(classification_report(y_test, y_pred_l1, target_names=["no", "yes"], digits=4))

y_probs_l1 = log_reg_l1.predict_proba(X_test_scald)[:, 1] # Probabilities for class 1

roc_auc_l1 = roc_auc_score(y_test, y_probs_l1)

print(f"ROC AUC Score: {roc_auc_l1:.4f}")

# L2 regularization

start_fit = time.perf_counter()

log_reg_l2.fit(X_train_scald, y_train)

end_fit = time.perf_counter()

start_pred = time.perf_counter()

y_pred_l2 = log_reg_l2.predict(X_test_scald)

end_pred =time.perf_counter()

cm_l2 = confusion_matrix(y_test, y_pred_l2, labels=[0,1])

print("L2 regularisation results:")

print(classification_report(y_test, y_pred_l2, target_names=["no", "yes"], digits=4))

y_probs_l2 = log_reg_l2.predict_proba(X_test_scald)[:, 1] # Probabilities for class 1

roc_auc_l2 = roc_auc_score(y_test, y_probs_l2)

print(f"ROC AUC Score: {roc_auc_l2:.4f}")

# Report timings

log_reg_l2_fit_time = end_fit - start_fit

log_reg_l2_pred_time = end_pred - start_pred

print(f"Log Regression (L2) fitting time: {log_reg_l2_fit_time:.4f} seconds")

print(f"Log Regression (L2) prediction time: {log_reg_l2_pred_time:.4e} seconds")

# Plotting function

def plot_confusion_matrix(cm, title, ax):

sns.heatmap(cm, annot=True, fmt='d', cmap='Blues', cbar=False, ax=ax)

ax.set_title(title)

ax.set_xlabel('Predicted')

ax.set_ylabel('Actual')

ax.set_xticklabels(['no', 'yes'])

ax.set_yticklabels(['no', 'yes'])

# Create subplots

fig, axes = plt.subplots(1, 3, figsize=(18, 5))

plot_confusion_matrix(cm_nr, 'No Regularization', axes[0])

plot_confusion_matrix(cm_l1, 'L1 Regularization', axes[1])

plot_confusion_matrix(cm_l2, 'L2 Regularization', axes[2])

plt.tight_layout()

plt.show()L1 regularisation results:

precision recall f1-score support

no 0.9319 0.9093 0.9205 7985

yes 0.4213 0.4981 0.4565 1058

accuracy 0.8612 9043

macro avg 0.6766 0.7037 0.6885 9043

weighted avg 0.8721 0.8612 0.8662 9043

ROC AUC Score: 0.7738

L2 regularisation results:

precision recall f1-score support

no 0.9319 0.9088 0.9202 7985

yes 0.4204 0.4991 0.4564 1058

accuracy 0.8609 9043

macro avg 0.6762 0.7039 0.6883 9043

weighted avg 0.8721 0.8609 0.8660 9043

ROC AUC Score: 0.7736

Log Regression (L2) fitting time: 0.5195 seconds

Log Regression (L2) prediction time: 1.3113e-03 seconds

feature_names = X_train.columns

coefs_nr = log_reg_nr.coef_.flatten()

coefs_l1 = log_reg_l1.coef_.flatten()

coefs_l2 = log_reg_l2.coef_.flatten()

logistic_nr = pd.DataFrame({'feature_name': feature_names, 'coefficients': coefs_nr})

logistic_l1 = pd.DataFrame({'feature_name': feature_names, 'coefficients': coefs_l1})

logistic_l2 = pd.DataFrame({'feature_name': feature_names, 'coefficients': coefs_l2})

results = [logistic_nr, logistic_l1, logistic_l2]

fig, axes = plt.subplots(3, 1, figsize=(8, 21))

subplot_titles=["No regularisation", "L1 regularisation", "L2 regularisation"]

for i, ax in enumerate(axes):

# Sort the features by the absolute value of their coefficient

results[i]["abs_value"] = results[i]["coefficients"].apply(lambda x: abs(x))

#results[i]["colors"] = results[i]["coefficients"].apply(lambda x: "green" if x > 0 else "red")

results[i] = results[i].sort_values("abs_value", ascending=False)

sns.barplot(x="feature_name", y="coefficients", data=results[i].head(20),ax=ax)

# Colour bars based on coefficient sign

for bar, coeff in zip(ax.patches, results[i]['coefficients']):

bar.set_color('green' if coeff >= 0 else 'red')

axes[i].set_xlabel("Feature Name", fontsize=12)

tick_positions = range(20)

ax.set_xticks(tick_positions)

ax.set_xticklabels(results[i]["feature_name"].head(20), rotation=45, ha='right')

axes[i].set_ylabel("Coef", fontsize=12)

axes[i].tick_params(axis='x', labelrotation=45)

ax.set_title(subplot_titles[i])

# Rotate x-axis labels for better readability

plt.xticks(rotation=45, ha='right')

fig.suptitle("Top 20 Features Logistic Regression", fontsize=14)

plt.tight_layout(rect=[0, 0, 1, 0.99])

plt.show()

# Compare feature selection between L1 and L2

print(f"L1 non-zero features: {np.sum(log_reg_l1.coef_[0] != 0)}")

print(f"L2 non-zero features: {np.sum(log_reg_l2.coef_[0] != 0)}")

print(f"Total features: {len(log_reg_l1.coef_[0])}")L1 non-zero features: 43

L2 non-zero features: 47

Total features: 47print("Features removed from L1 model:")

logistic_l1[logistic_l1["coefficients"] == 0]Features removed from L1 model:| feature_name | coefficients | abs_value | |

|---|---|---|---|

| 16 | job_technician | 0.0 | 0.0 |

| 19 | marital_divorced | 0.0 | 0.0 |

| 39 | month_may | 0.0 | 0.0 |

| 46 | poutcome_unknown | 0.0 | 0.0 |

from sklearn.metrics import precision_recall_curve

from sklearn.metrics import roc_curve

yRawScores_nr = log_reg_nr.decision_function(X_train_scald)

yRawScores_l1 = log_reg_l1.decision_function(X_train_scald)

yRawScores_l2 = log_reg_l2.decision_function(X_train_scald)

fpr_nr, tpr_nr, thresholds_nr = roc_curve(y_train, yRawScores_nr)

fpr_l1, tpr_l1, thresholds_l1 = roc_curve(y_train, yRawScores_l1)

fpr_l2, tpr_l2, thresholds_l2 = roc_curve(y_train, yRawScores_l2)

plt.figure(figsize=(8,8))

plt.plot(fpr_nr,tpr_nr, label="no regularisation")

plt.plot(fpr_l1,tpr_l1, label="L1 regularisation")

plt.plot(fpr_l2,tpr_l2, label="L2 regularisation")

plt.xlabel("FPR",fontsize=15)

plt.ylabel("Recall (TPR)",fontsize=15)

plt.title("ROC",fontsize=20)

randomAssignment = np.random.normal(size=len(y_train))

fprRand, tprRand, thresholdsRand = roc_curve(y_train, randomAssignment)

plt.plot(fprRand, tprRand, ls="--", label="random classifier")

plt.legend()

plt.show()

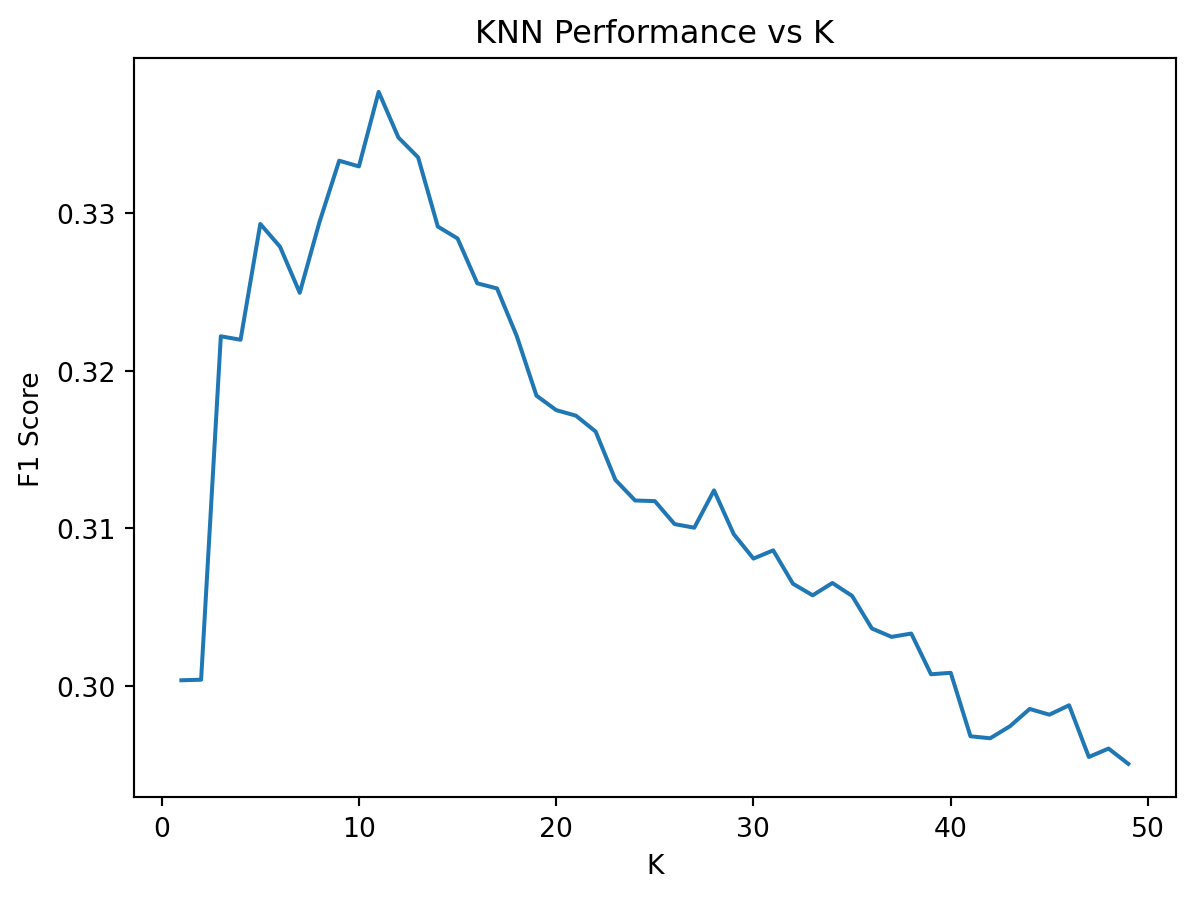

K-Nearest-Neighbour (KNN)

In this section, I fit a KNN model to the data. First, I use a grid search to find the optimal settings for K, the number of neighbours and the weights. The scoring of the model uses the F1 score to be consistent with the Logistic regression model produced earlier in this work.

from sklearn.neighbors import KNeighborsClassifier

from sklearn.model_selection import GridSearchCV

from sklearn.pipeline import Pipeline

import numpy as np

# Create pipeline

pipeline = Pipeline([

('knn', KNeighborsClassifier())

])

# Define K range to search

n_samples = len(X_train_scald)

sqrt_n = int(np.sqrt(n_samples))

# Test around this value

k_range = list(range(1, min(sqrt_n * 2, 50)))

param_grid = {

'knn__n_neighbors': k_range,

'knn__weights': ['uniform', 'distance'],

}

# Grid search with CV

knn_grid_search = GridSearchCV(

pipeline,

param_grid,

cv=5,

scoring='f1',

n_jobs=-1

)

knn_grid_search.fit(X_train_scald, y_train)

print(f"Best K: {knn_grid_search.best_params_}")

print(f"Best Score: {knn_grid_search.best_score_:.4f}")Best K: {'knn__n_neighbors': 11, 'knn__weights': 'distance'}

Best Score: 0.3377import matplotlib.pyplot as plt

from sklearn.model_selection import cross_val_score

# Extract results

k_scores = []

for k in k_range:

knn = KNeighborsClassifier(n_neighbors=k, weights="distance")

scores = cross_val_score(knn, X_train_scald, y_train, cv=5, scoring="f1")

k_scores.append(scores.mean())

plt.plot(k_range, k_scores)

plt.xlabel("K")

plt.ylabel("F1 Score")

plt.title("KNN Performance vs K")

plt.show()

knn_model = KNeighborsClassifier(n_neighbors=11, weights="distance")

start_fit = time.perf_counter()

knn_model.fit(X_train_scald, y_train)

end_fit = time.perf_counter()

start_pred = time.perf_counter()

y_pred_knn = knn_model.predict(X_test_scald)

end_pred = time.perf_counter()

print(classification_report(y_test, y_pred_knn, target_names=["no", "yes"], digits=4))

y_probs_knn = knn_model.predict_proba(X_test_scald)[:, 1] # Probabilities for class 1

roc_auc_knn = roc_auc_score(y_test, y_probs_knn)

print(f"ROC AUC Score: {roc_auc_knn:.4f}")

# Report timings

knn_fit_time = end_fit - start_fit

knn_pred_time = end_pred - start_pred

print(f"KNN fitting time: {knn_fit_time:.4f} seconds")

print(f"KNN prediction time: {knn_pred_time:.4f} seconds") precision recall f1-score support

no 0.9077 0.9752 0.9402 7985

yes 0.5733 0.2514 0.3495 1058

accuracy 0.8905 9043

macro avg 0.7405 0.6133 0.6449 9043

weighted avg 0.8686 0.8905 0.8711 9043

ROC AUC Score: 0.7391

KNN fitting time: 0.0062 seconds

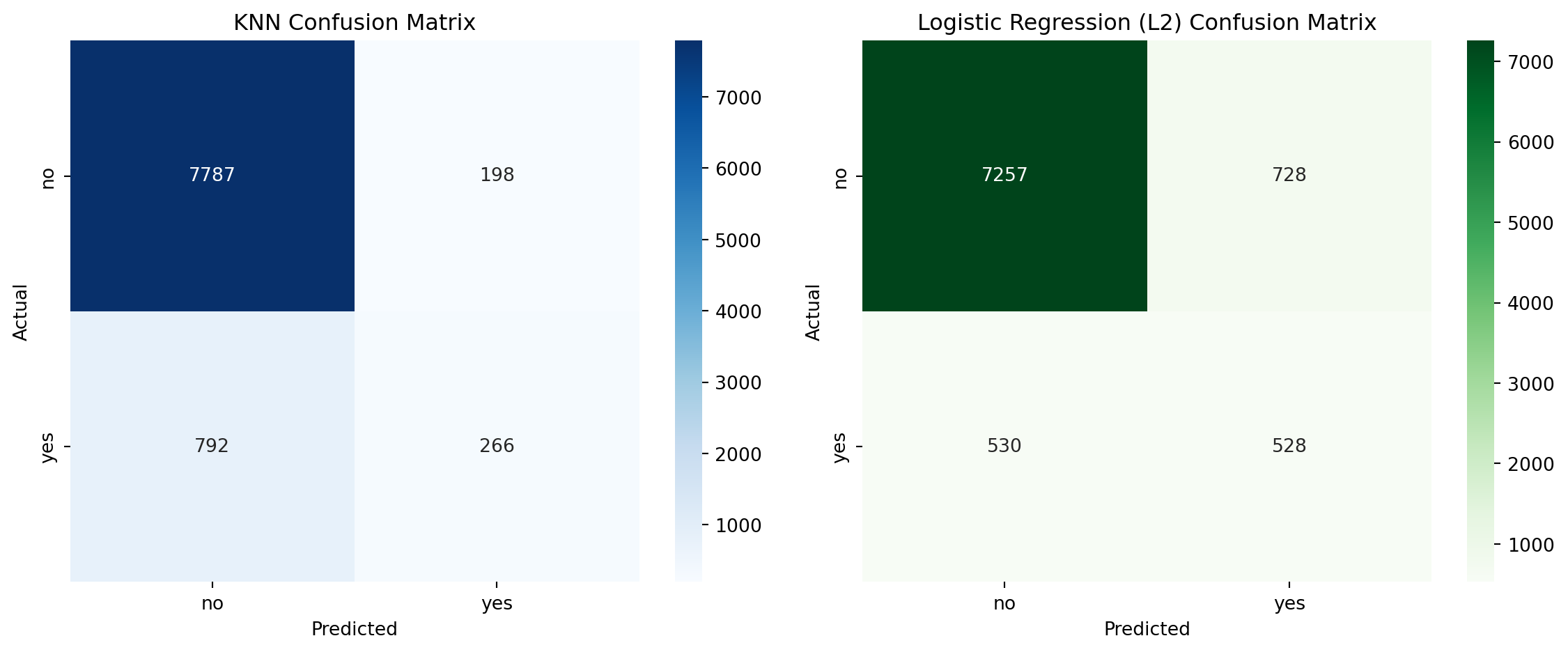

KNN prediction time: 0.6241 secondsComparsion between Logistic regression and KNN models

# Calculate confusion matrix for KNN

knn_cm = confusion_matrix(y_test, y_pred_knn, labels=[0,1])

# Plot confusion matrices

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

labels = ['no', 'yes']

# KNN Confusion Matrix

sns.heatmap(knn_cm, annot=True, fmt='d', cmap='Blues', ax=axes[0])

axes[0].set_title('KNN Confusion Matrix')

axes[0].set_xlabel('Predicted')

axes[0].set_ylabel('Actual')

axes[0].set_xticklabels(labels)

axes[0].set_yticklabels(labels)

# Logistic Regression Confusion Matrix

sns.heatmap(cm_l2, annot=True, fmt='d', cmap='Greens', ax=axes[1])

axes[1].set_title('Logistic Regression (L2) Confusion Matrix')

axes[1].set_xlabel('Predicted')

axes[1].set_ylabel('Actual')

axes[1].set_xticklabels(labels)

axes[1].set_yticklabels(labels)

plt.tight_layout()

plt.show()

Performance Comparison: KNN vs Logistic Regression

Minority class (“yes”) metrics

| Metric | Logistic Regression (L2) | KNN |

|---|---|---|

| Precision | 0.4204 | 0.5733 |

| Recall | 0.4991 | 0.2514 |

| F1 Score | 0.4564 | 0.3495 |

Observation: KNN has low recall for the “yes” class, meaning it misses most of the actual positive cases. This is critical in marketing, where identifying potential responders is key. It does have higher precision, which means less time would be wasted on potential “no” responders.

Overall metrics

| Metric | Logistic Regression (L2) | KNN |

|---|---|---|

| Accuracy | 0.8609 | 0.8905 |

| Macro F1 | 0.6883 | 0.6449 |

| Weighted F1 | 0.8663 | 0.8711 |

| ROC_AUC | 0.7736 | 0.7391 |

Observation: KNN performs well on the majority class (“no”) but poorly on the minority class (“yes”), dragging down macro and weighted averages.

Training time

| Model | Training Time (s) | Prediction Time (s) |

|---|---|---|

| Logistic Regression (L2) | 0.1785 | 1.154200e-03 |

| KNN | 0.01 | 0.3590 |

KNN is faster at training because it simply stores the numbers and doesn’t do any calculations. However, it is much slower at prediction, because it does the calculations at that point. Based on the sum of training and prediction, Logistic Regression is faster overall.

Number of trainable parameters

| Model | Trainable Parameters |

|---|---|

| Logistic Regression | Weights for each feature (plus bias). For binary classification with n features, it learns n + 1 parameters. |

| KNN | Stores the training data and makes decisions at prediction time, and has no trainable parameters. |

Logistic Regression is more compact and interpretable.

Conclusion

For this application, KNN was worse than Logistic Regression because:

- KNN was worse at identifying “yes” cases, which is crucial in marketing.

- KNN had a faster training time but slower prediction time. This was noticeable when testing SMOTE (not shown in this notebook).